: Latest Facts on Genetic Testing")

Our team gathered data from a mix of peer-reviewed research, federal regulatory disclosures, market-research reports, company filings, and consumer surveys published between 2023 and 2026. All sources were reviewed in May 2026.

We compiled data on the following:

- Latest market trends and forecasts on the DNA testing industry

- Current and future demand for genetic testing services

- Number and percentage of companies providing DNA tests

- DNA database size of the largest DNA companies

- Demographics and consumer opinion around DNA testing

- The 2025 23andMe bankruptcy and what happened to customer data

- FDA regulation of direct-to-consumer (DTC) genetic tests

Where statistics rely on older surveys, we explicitly label the vintage so you can judge currency for yourself.

Market Trends in DNA Testing

Demand for genetic tests has grown steadily over the past decade, even as the at-home DNA testing landscape has consolidated around fewer providers. The market splits into several distinct buckets: clinical genetic testing, consumer genomics, and direct-to-consumer (DTC) genetic testing. Each has its own size and trajectory.

Global Market Trends in Genetic Testing

- In 2025, the global genetic testing market reached an estimated $37.32 billion. It’s projected to grow to $93.94 billion by 2034, at a compound annual growth rate (CAGR) of 10.85% from 2026 to 2034.

- The broader consumer genomics market (which includes ancestry, traits, wellness, and health DNA products sold directly to individuals) was valued at $2.03 billion in 2024 and is forecast to reach $18.83 billion by 2034.

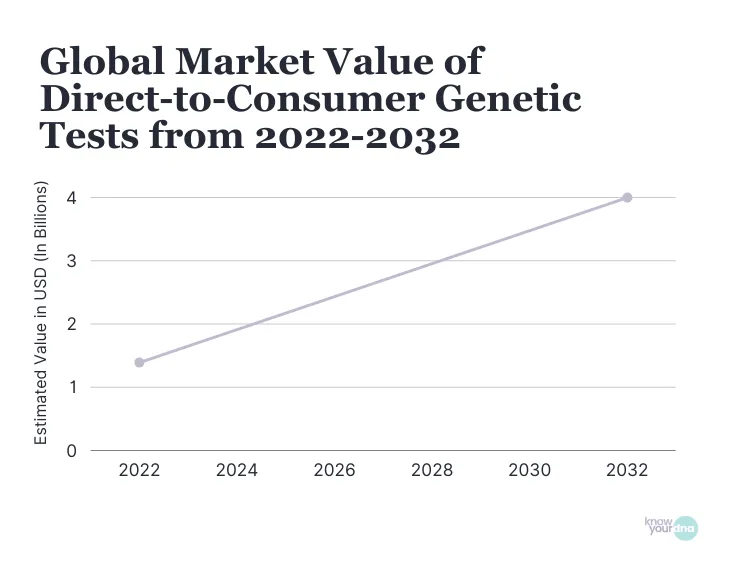

- The DTC genetic testing market (a narrower slice of consumer genomics, focused on tests sold without a clinician’s order) was estimated at $2.36 billion in 2024 and $2.79 billion in 2025. Industry analysts project it to reach $8.73 billion by 2032, with a forecast CAGR of about 17.7%.

- A separate analyst track puts the global DTC market at $2.17 billion in 2025 and forecasts $11.02 billion by 2035.

A note on those figures: “clinical genetic testing,” “consumer genomics,” and “DTC” describe different markets and shouldn’t be compared directly. The forecasts above come from industry-research firms (Fortune Business Insights, Precedence Research, Research and Markets), useful for direction, but treat the exact numbers as ranges.

At-Home DNA Testing in the U.S. & Other Countries

- The U.S. consumer genomics market was valued at $661.7 million in 2024.

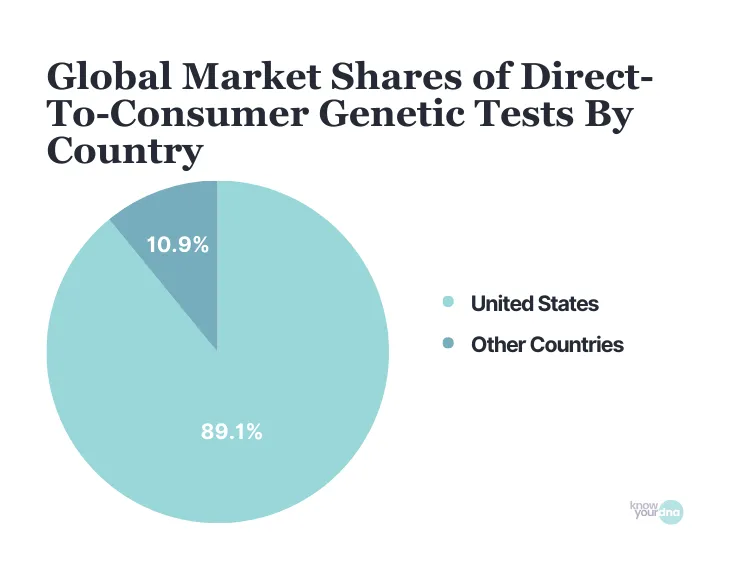

- The U.S. DTC genetic testing market reached $1.01 billion in 2025, making the U.S. the world’s largest single-country DTC market.

- The U.S. continues to dominate North American consumer DNA testing, driven by a saturated retail channel (Amazon, big-box, pharmacy) and a long tail of mid-priced ancestry and wellness products.

- China is the second-largest national consumer-genomics market, anchored by local providers like WeGene and 23mofang. Combined customer-base disclosures from Chinese providers are limited, so we no longer publish a specific Chinese market-share figure here.

Market Trends for Types of DTC Genetic Testing

The global market for direct-to-consumer DNA testing is built on three types of test technology:

- Single nucleotide polymorphism (SNP) chips

- Targeted analysis

- Whole genome sequencing (WGS)

SNP chips (the technology behind most ancestry and health kits from companies like AncestryDNA and 23andMe) have historically held the largest share of the DTC market by test volume. They’re inexpensive to run, fast to genotype, and well-suited to ancestry and traits products. Whole genome sequencing, offered by newer entrants like Nebula Genomics (whose consumer product line evolved in 2024 to focus on DNA Complete) and Nucleus Genomics, is gaining ground as sequencing costs drop, but it’s still a smaller slice of the consumer market because the price per kit remains higher than SNP-based products.

Demand for At-Home DNA Tests

Several long-running drivers continue to support at-home DNA test demand:

- Wider public awareness of consumer DNA products through TV, social media, and gift-giving cycles

- Growing demand for personalized genetics, traits, and wellness products

- Rising public interest in inherited-disease risk after high-profile cases involving cancer and hereditary heart conditions, plus separate interest in pharmacogenomics (how your genes affect the way your body processes certain medications)

- Lower kit prices, which have made at-home DNA testing accessible to households that wouldn’t have considered it a decade ago

That said, demand has cooled from its 2018–2019 peak. After the 2023 23andMe data breach and the company’s 2025 Chapter 11 filing, consumer trust took a measurable hit, a shift visible in the YouGov polling further down this page.

A 2024 peer-reviewed policy analysis in the Journal of Medical Internet Research framed the trade-off this way: DTC genetic testing offers clear benefits (earlier identification of disease risk and greater consumer engagement with personal health) alongside ongoing concerns about test quality, result interpretation, and data privacy.

Companies Providing At-Home DNA Tests

The leading at-home genetic testing companies in the U.S. are AncestryDNA, 23andMe, MyHeritage, and Family Tree DNA. In China, WeGene and 23mofang remain the two largest providers of direct-to-consumer genetic tests, though current combined customer-count disclosures from Chinese providers are limited.

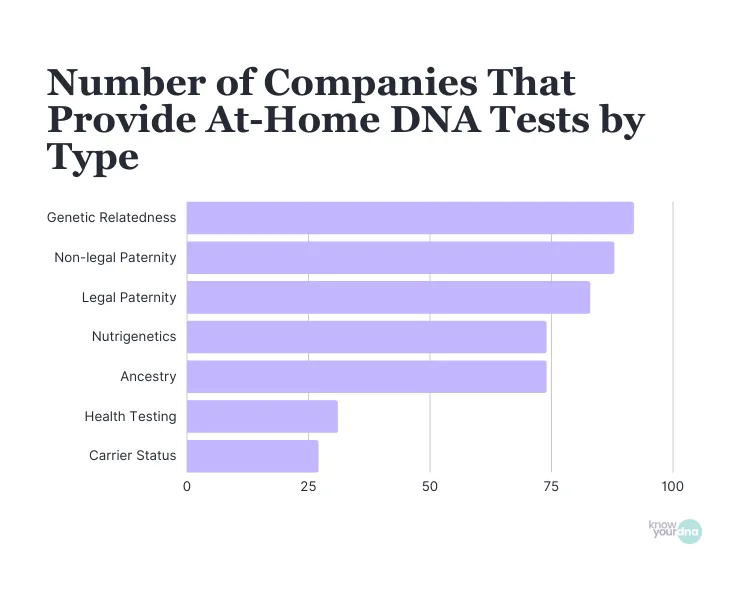

DTC kits cluster around a handful of use cases:

- Genetic ancestry estimates (often marketed as “ethnicity estimates”) that compare your DNA to reference panels of self-identified populations

- Genetic relatedness and family matching (including paternity testing)

- Nutrigenetics and “diet & wellness” reports

- Health risk reports (for tests authorized by the FDA to do so)

- Carrier status screening for inherited conditions

The FDA splits DTC tests into a few different buckets. Ancestry tests aren’t reviewed by the FDA before marketing. Low-risk general-wellness products generally aren’t either. Moderate- to high-risk medical uses (genetic health-risk reports, cancer-predisposition claims, and similar) are subject to FDA review, clearance, or authorization. Carrier screening sits in between, with specific requirements but no across-the-board premarket review. We cover the regulatory landscape further down this page.

A newer wave of whole-genome sequencing providers (Nebula Genomics, Nucleus Genomics, Orchid, and others) has also entered the consumer market with a different price-and-product mix than the SNP-chip incumbents.

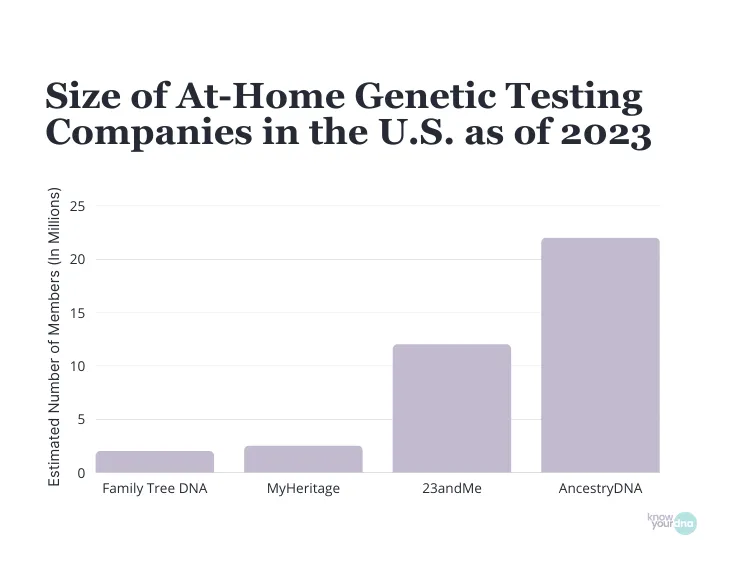

DNA Database Size of Testing Companies

AncestryDNA remains the world’s largest consumer DNA network. Ancestry’s own corporate Company Facts page reports over 30 million people in its consumer DNA network as of 2026.

23andMe last publicly reported more than 14 million genotyped customers in its FY2023 financial results. The company did not publish an updated live-customer count before its 2025 Chapter 11 filing, so the 14 million figure is the most recent self-reported number we’ll cite, not a current 2026 active-customer count.

MyHeritage and Family Tree DNA round out the major U.S. consumer DNA networks. Independent industry tracker The DNA Geek estimates MyHeritage at roughly 9.6 million and Family Tree DNA at just under 1.8 million kits or database entries as of March 2026. Treat those as third-party estimates rather than company-confirmed numbers, as neither company publishes its current customer count on a fixed schedule, and The DNA Geek’s figures include uploads from other services.

In China, WeGene and 23mofang have continued to grow, but neither has published a recent combined-database figure in English-language disclosures, so we no longer publish a specific Chinese figure here.

The 23andMe Bankruptcy and What Happened to Customer DNA Data

On March 23, 2025, 23andMe filed for voluntary Chapter 11 bankruptcy protection. The filing followed years of declining test sales, a major October 2023 data breach that exposed information tied to roughly 6.9 million customers, sustained losses from a foray into drug development, and a failed take-private bid by co-founder Anne Wojcicki.

The bankruptcy raised an immediate question for the company’s roughly 14 million customers: what would happen to their genetic data? California Attorney General Rob Bonta issued an urgent consumer alert reminding 23andMe customers of their right to delete genetic data and saliva samples under California’s Genetic Information Privacy Act. Other state attorneys general and the FTC followed with similar guidance.

On July 14, 2025, TTAM Research Institute (a nonprofit public benefit corporation founded by Anne Wojcicki) completed its acquisition of 23andMe’s assets through the court-approved sale process. The TTAM agreement included several customer-data commitments:

- Existing customer consent agreements and deletion rights carried over to TTAM

- Customer notification ahead of the asset transfer

- Restrictions on bulk data transfers to third parties

- A privacy advisory board and reporting procedures

- Reaffirmed opt-out rights for research participation

The 23andMe collapse is the largest single disruption in the DTC genetic-testing industry to date and has reshaped how customers, regulators, and competitors think about long-term data stewardship.

People Who Have Taken A Home DNA Test (Global)

By early 2019, more than 26 million consumers were in the four leading commercial ancestry and health DNA databases, per MIT Technology Review’s widely cited tally, the figure that anchored most reporting on consumer DNA adoption through the early 2020s.

The 2026 number is meaningfully higher. Combining the publicly disclosed or third-party-estimated database sizes for the six major at-home DNA providers:

- AncestryDNA: over 30 million people (company-reported, 2026)

- 23andMe: approximately 14 million genotyped customers (last reported FY2023; post-bankruptcy count not separately disclosed)

- MyHeritage: approximately 9.6 million kits/database entries (third-party estimate, March 2026)

- Family Tree DNA: approximately 1.8 million kits/database entries (third-party estimate, March 2026)

- WeGene and 23mofang (China): combined customer-base disclosures are limited; Chinese local providers have continued to grow

Adding the disclosed and estimated counts yields a working total of roughly 55 to 60 million database memberships or kits across the major named providers. That’s not a direct count of unique people. The underlying numbers mix three different units (Ancestry’s “people,” 23andMe’s “genotyped customers,” and The DNA Geek’s kit/database estimates, which include uploads from other services), and a meaningful share of consumers have tested with or uploaded to more than one database. The true number of individuals who have ever taken a home DNA test is somewhat lower than the database total.

Americans Who Have Taken An At-Home Genetic Test

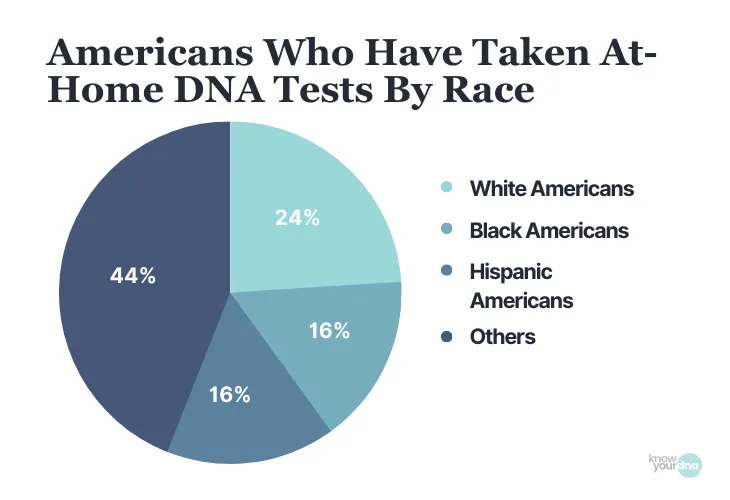

A 2025 YouGov survey of U.S. adults found that about 21% of Americans have taken a home DNA test, roughly consistent with prior YouGov rounds, suggesting market penetration has stabilized at around one in five rather than continued to climb. Key demographic findings:

- Close family-member testing extends DNA-test exposure to a much larger share of Americans.

- White Americans remain more likely to have taken an at-home DNA test than Black or Hispanic Americans, a longstanding pattern tied in part to reference-panel coverage and marketing reach.

- Older Americans test at higher rates than younger ones; adults 50 and over remain the most-tested age group.

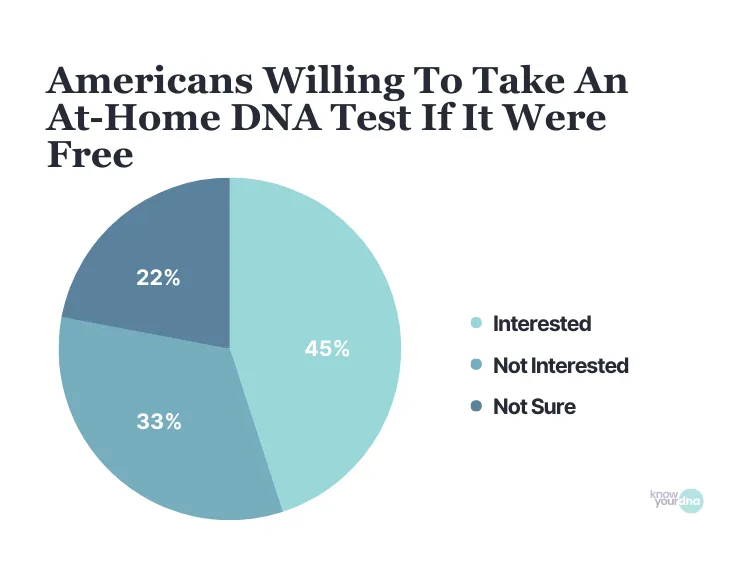

American Interest in At-Home Genetic Tests

Most Americans who haven’t taken a DNA test still say they’d consider one. In YouGov’s 2025 tracking, respondents who were interested in a test cited similar reasons to past years:

- Learning about family origin and ancestry remains the top reason.

- Health and family medical history is the second-most-cited driver.

- Connecting with previously unknown biological relatives is a recurring third reason.

Privacy concerns are now the single most-cited reason respondents would decline to take a test, a shift from earlier YouGov rounds when cost and skepticism about accuracy were more prominent.

Willingness To Take A DNA Test

Surveyed Americans say they’d be more likely to take a DNA test under specific circumstances:

- If it helped them estimate their chance of developing a serious health condition

- If they were adopted or didn’t know one biological parent

- If they had a biological sibling they’d never met

- If they wanted to know more about a specific ancestor or family-history question

- If a doctor recommended a clinical genetic test for a specific reason

Across both at-home and clinical genetic testing, doctor recommendation remains the strongest single motivator, more powerful than friend or family-member testimonials, media coverage, or public-figure endorsements. Privacy assurances and the cost of the test are also recurring factors in whether Americans say they’d test.

Adopted vs. Non-Adopted Americans

YouGov’s adoption-specific subgroup is small (typically around 5% of the U.S. sample), but the pattern is consistent across years: adopted Americans are roughly twice as likely as non-adopted Americans to have taken an at-home DNA test (about 36% vs. 20% in earlier YouGov rounds).

Among adopted Americans who have tested:

- More than half said it helped them learn more about a close relative.

- About 1 in 3 said DNA testing made them rethink their race or ethnicity.

- A meaningful minority said it connected them to their birth families.

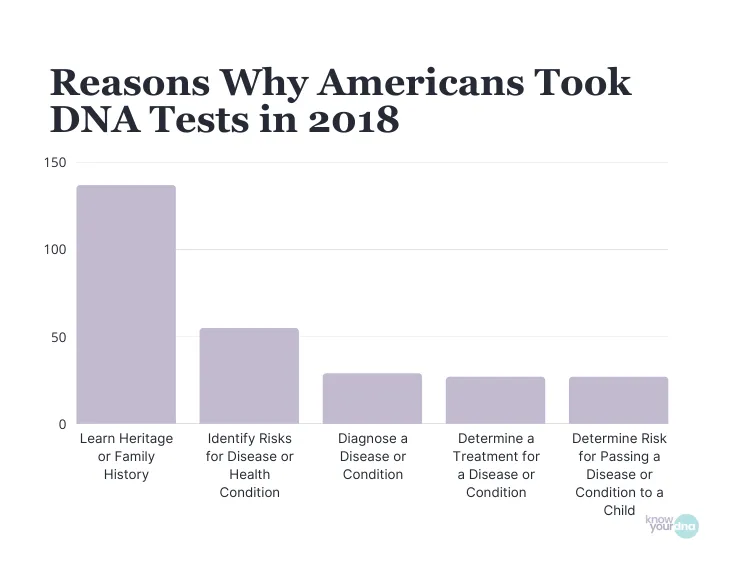

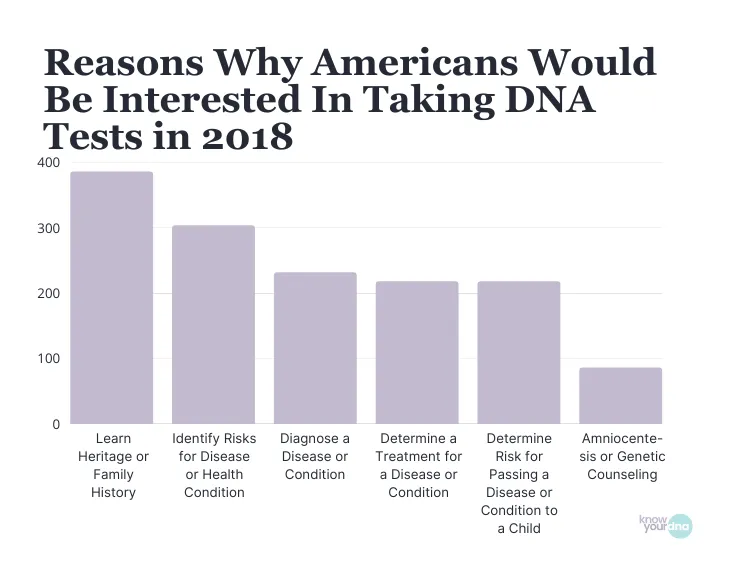

Why Americans Take DNA Tests

In YouGov’s 2025 tracking, the top reasons U.S. adults give for taking (or wanting to take) a genetic test are:

- Heritage and family history: by far the most-cited reason

- Knowing their risk of an inherited disease or condition

- Identifying the best treatment for an existing health condition

- Diagnosing a specific disease or condition

- Knowing whether they could pass an inherited condition to their children

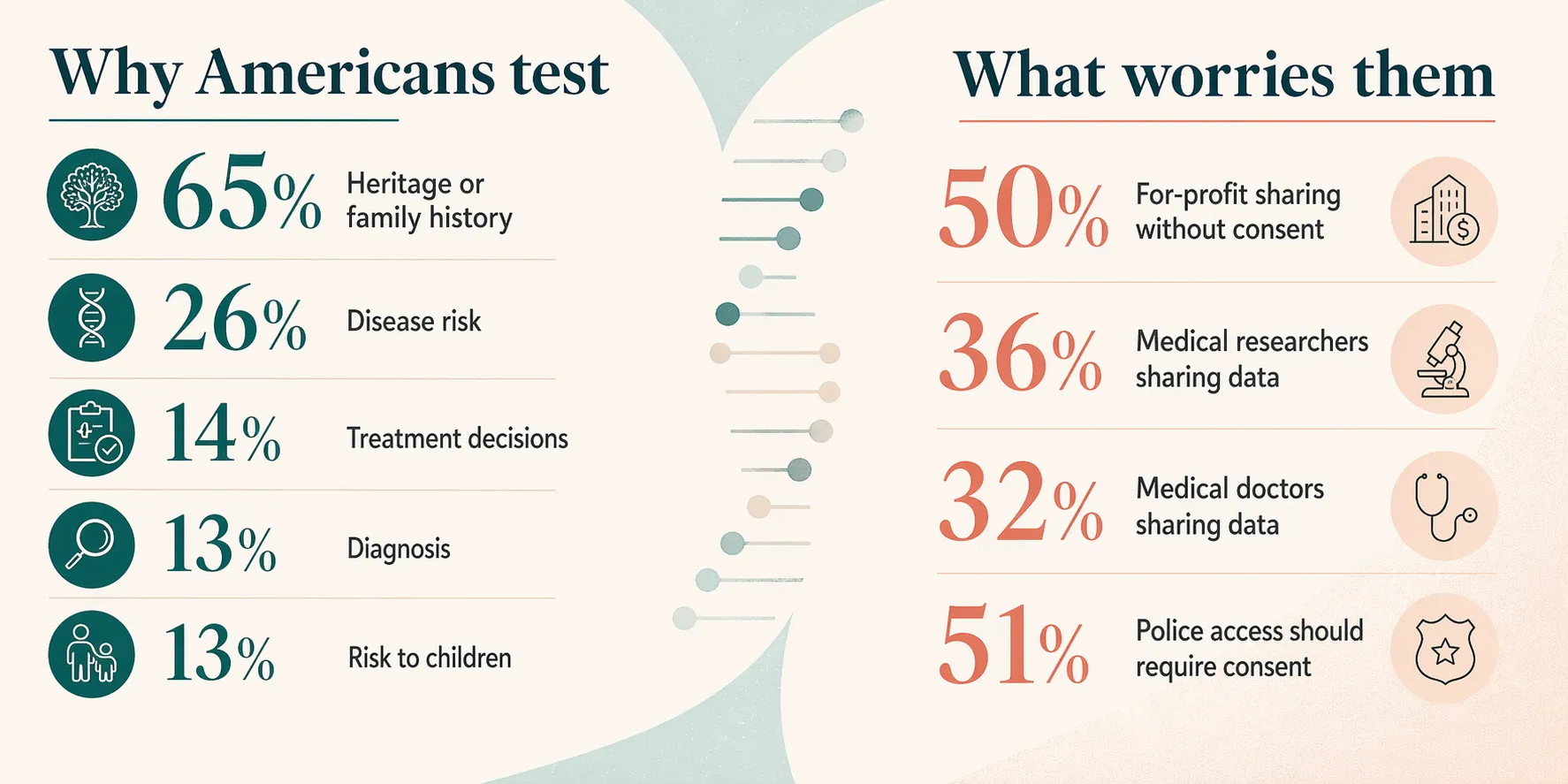

For historical comparison, an earlier 2018 AP-NORC poll of 210 adults who had taken a genetic test found a similar rank order: 65% cited heritage, 26% disease risk, 14% treatment guidance, 13% diagnosis, and 13% knowing whether they could pass on an inherited condition.

The same 2018 AP-NORC poll surveyed 454 adults who hadn’t tested yet. Their motivations followed a similar pattern: 85% cited heritage, 67% disease risk, 51% diagnosis of a specific condition, 48% knowing whether they could pass on an inherited condition, 48% treatment guidance, and 19% prenatal-related reasons.

Public interest in DNA tests for diagnosing a specific condition has softened in newer YouGov rounds as awareness grows that consumer DNA kits aren’t diagnostic tools. That’s a job for clinical genetic testing, often coordinated through a genetic counselor.

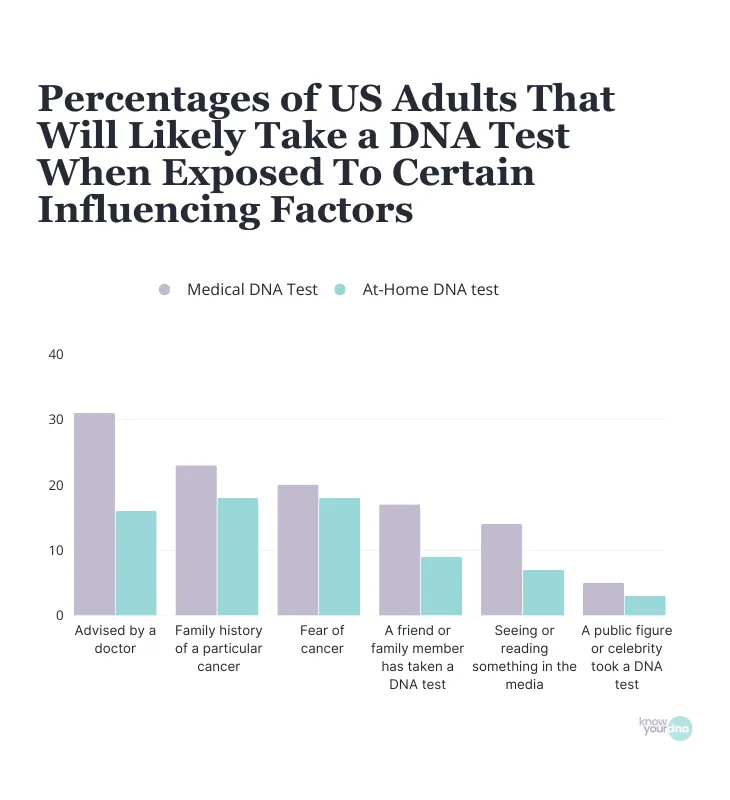

Factors That Affect The Likelihood of Taking A DNA Test

Different factors drive people toward clinical genetic tests versus at-home kits. Per the 2018 AP-NORC poll, American adults were more likely to choose a medical DNA test over an at-home one when a doctor advised it (31% vs. 16%), when they had a family history of a particular cancer (23% vs. 18%), or when they had a general fear of cancer (20% vs. 18%).

By contrast, Americans tended to prefer at-home DNA tests when a friend or family member had taken one (17% vs. 9%), when they read about DNA testing in the media (14% vs. 7%), or when a public figure they followed had taken a genetic test (5% vs. 3%).

In other words: clinical testing is medically motivated and provider-directed; at-home testing is socially motivated and consumer-directed. Both have a place; the cost of genetic testing article walks through the price differences between the two paths.

FDA Regulation of DTC Genetic Tests

The FDA regulates direct-to-consumer genetic tests when they make moderate- to high-risk health claims: disease risk, cancer predisposition, or pharmacogenomic information about how your genes may affect medication response. Ancestry tests and low-risk general-wellness products generally aren’t reviewed by the FDA before they hit the market. Carrier screening sits in between, with specific requirements but no across-the-board premarket review.

A quick regulatory glossary, because these terms get used interchangeably and they shouldn’t:

- PMA approval (“FDA approved”): the highest premarket-review bar, reserved for the highest-risk devices. Rare for consumer genetic tests.

- De Novo authorization (“FDA authorized”): the path for novel low-to-moderate-risk devices without a clear predicate. 23andMe’s health-risk reports for hereditary conditions like BRCA1/BRCA2 mutations, for example, are FDA authorized, not approved.

- 510(k) clearance (“FDA cleared”): for devices that are substantially equivalent to an existing predicate device.

- No FDA action: many DTC tests for ancestry, relatedness, and traits fall outside FDA jurisdiction entirely.

The lab-developed tests (LDT) rule has had a turbulent two years. In May 2024, the FDA finalized an LDT Final Rule that would have brought many lab-developed tests (including those used by some DTC genetic-testing companies) under FDA premarket review, quality-system regulations, and adverse-event reporting, with compliance phased in through 2028. On March 31, 2025, a federal district court vacated that rule. The FDA then issued a new final rule on September 19, 2025, restoring the pre-2024 regulatory text. As of May 2026, the 2024 LDT phase-in is not in effect, and lab-developed tests are back under the FDA’s earlier framework. The agency has signaled it’s still considering its options for future LDT oversight.

Through 2024, 2025, and into 2026, the FDA has continued to use warning letters and post-market surveillance to address DTC tests that make unauthorized health claims or fail to report safety events. Specific enforcement actions are tracked through the FDA Warning Letters database.

A peer-reviewed 2024 study in the Journal of Medical Internet Research provides a framework for evaluating DTC genetic testing services across benefits, risks, quality, validity, and privacy, reinforcing the FDA’s caution that consumer DNA tests vary considerably in evidentiary support.

Common Concerns on DNA Testing

Privacy is the dominant concern in 2026, and the gap has widened since the 23andMe data breach and bankruptcy. The 2018 AP-NORC poll of 1,109 American adults remains a useful historical baseline, capturing a moment when consumer trust in DNA companies was meaningfully higher than it is today. In that poll, while up to 52% said they were interested in genetic testing, many were not fully convinced of the reliability of DTC tests for health applications.

Those concerns have not diminished since. The 2025 YouGov survey found that privacy concerns are now the leading reason Americans who haven’t tested cite for hesitating.

Sharing of Genetic Data

From the 2018 AP-NORC poll (historical baseline):

- 554 of 1,109 respondents (50%) were “extremely or very concerned” that for-profit DNA companies would share their genetic information without consent.

- 399 (36%) had the same level of concern about medical researchers handling their genetic data.

- 355 (32%) were extremely worried that medical doctors would share their data.

Those 2018 baseline numbers remain a useful reference point for the rank order of concerns (for-profit companies > medical researchers > doctors). YouGov’s 2025 tracking suggests the for-profit-company concern has moved higher post-bankruptcy. The directional reading is clear: 2018 was the peak of consumer trust in DTC DNA companies; 2026 is not. The TTAM acquisition of 23andMe’s assets is the first real-world test of whether customer consent agreements can survive a corporate-asset transfer. The consent-carryover and deletion-rights provisions in the TTAM deal are a direct response to these public concerns.

Access of Police to Genetic Information

From the 2018 AP-NORC poll:

- 566 (51%) of polled Americans believed genetic data should only be shared with the police if the person being tested consents.

- 366 (33%) said consent isn’t necessary for sharing genetic information with law enforcement.

- 144 (13%) completely opposed any use of consumer DNA data by police.

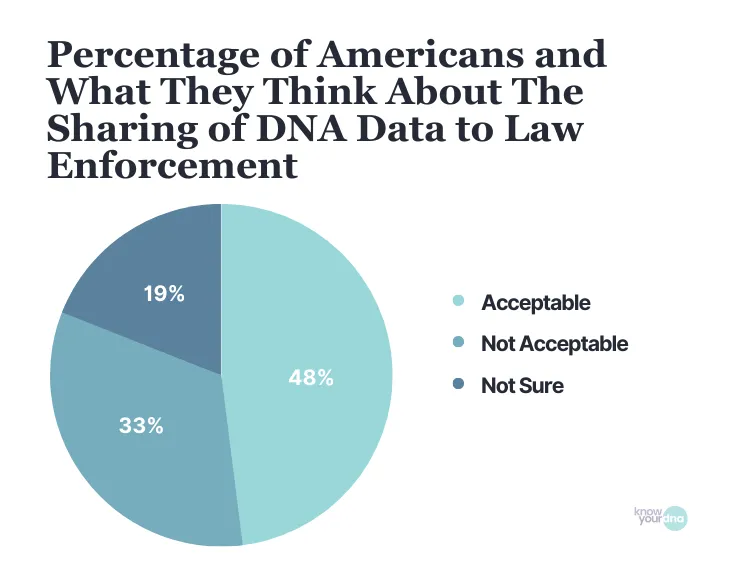

Pew Research Center’s 2020 tracking found a similar split, with about half of U.S. adults saying it’s acceptable for DNA testing companies to share customer data with law enforcement and about a third saying it’s unacceptable. We cover the law-enforcement-trust numbers in more detail below.

Reliability of At-Home DNA Tests

From the 2018 AP-NORC poll: about one-third of polled Americans thought at-home DNA tests are reliable for identifying inherited diseases or guiding treatment, and about 4 in 10 thought at-home DNA kits are reliable for identifying ethnic backgrounds, diagnosing diseases, or revealing carrier status.

These public perceptions reflect how people feel about the tests, not clinical assessments of their accuracy. The FDA’s guidance is more cautious: DTC tests vary in evidentiary support and purpose. If you’re considering a DNA test for health purposes, discussing the results with a genetic counselor or physician is the best way to understand what they do and don’t tell you.

American Trust in Sharing DNA Data with Law Enforcers

Pew Research Center’s 2020 tracking found that about 48% of U.S. adults said it was acceptable for DNA testing companies to share customer genetic data with law enforcement, while about 33% said it was unacceptable. Those numbers remain the most-cited baseline for the law-enforcement-access question.

The Pew data showed clear demographic splits:

- American women were more likely than American men to find it acceptable to share DNA information with law enforcement (about 53% vs. 43%).

- American adults aged 18 to 49 were likelier to find law-enforcement sharing unacceptable than those aged 50 and above (about 36% vs. 29%).

- A majority of Americans aged 50+ found law-enforcement sharing acceptable (about 56%); only about 29% of that age group found it unacceptable.

The 2018 Golden State Killer case (solved using genetic genealogy and a public DNA database) and the wave of similar cases since have kept this question visible. Public opinion has remained roughly stable.

Opinions on DNA Test Results

People who have taken a DNA test generally find their results useful, even when the results aren’t what they expected.

- Most who have tested say they find their results useful or helpful, around 85% in earlier polling.

- A majority (around 60%) would want to be informed if they had genetic variants linked to incurable diseases. A meaningful minority (around 39%) say they’d rather not know.

- The share of test-takers who’d tell their siblings or children about an inherited condition runs higher than 8 in 10 across polling waves (around 82% in earlier surveys).

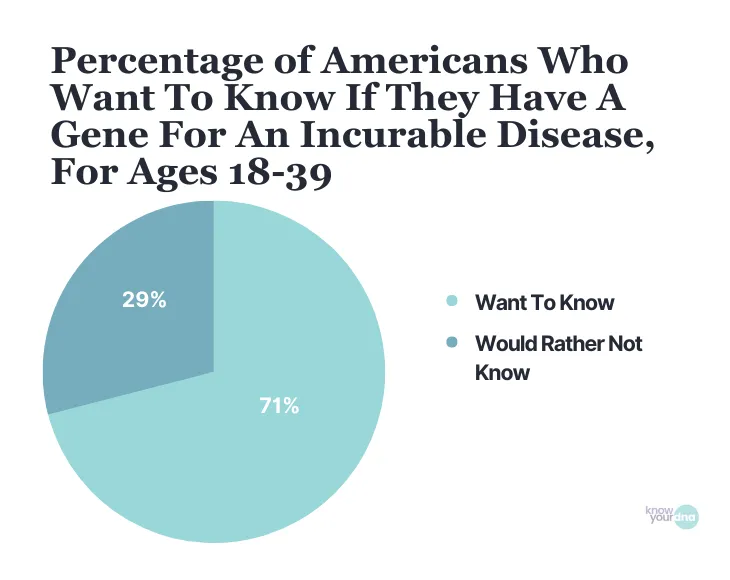

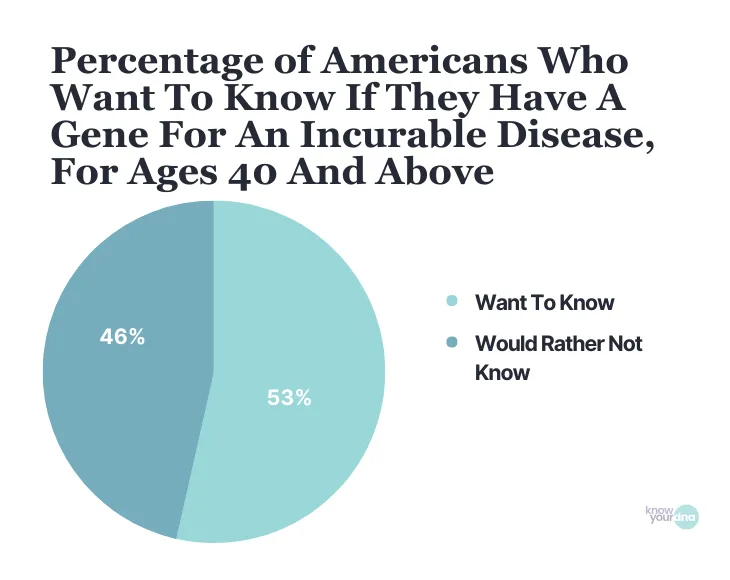

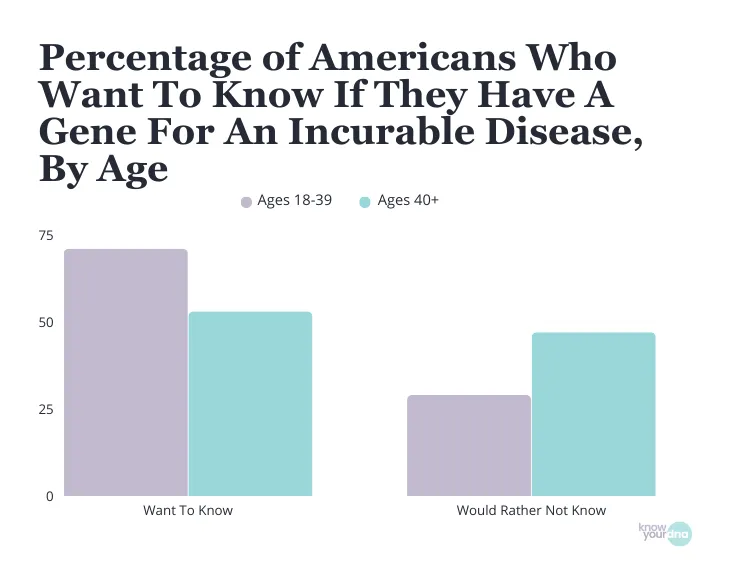

Younger American adults (those under 40) are generally more interested in learning their genetic predisposition to disease than older adults. Up to 71% of younger adults say they want to know if they’re at risk of developing a health condition, while adults 40 and over are more split: about 53% want to know, and about 46% would rather not. That generational pattern has held across multiple polling waves.

The 2025 YouGov wave shifted one thing: respondents are more likely than in past years to mention data privacy as a reason to be cautious about at-home DNA results. Technical accuracy is no longer the dominant concern. What happens to the data afterward is.